Zůstat

Zůstat

Obchodní podmínky

Nástroje

While most of the world's central banks, led by the Fed, continue to struggle with high inflation, the Bank of Japan is playing it cool. For years it has been unable to beat deflation, but global trends have pushed consumer prices in the Land of the Rising Sun up to 3.1%. There is now a reversal of supply shocks, which will slow inflation in most of the world. But will the BoJ have to fight low prices again?

In his speech to Parliament, Bank of Japan Governor Kazuo Ueda stated that he and his colleagues would abandon yield curve control in only one case. If the inflation forecast assumes that it is anchored near 2%, it will be possible to start cutting the balance sheet. Meanwhile, Ueda called the trend nature of inflation expectations as positive. The latter is growing. This suggests that the regulator continues to fight deflation, despite the rise in consumer prices to 3.1%.

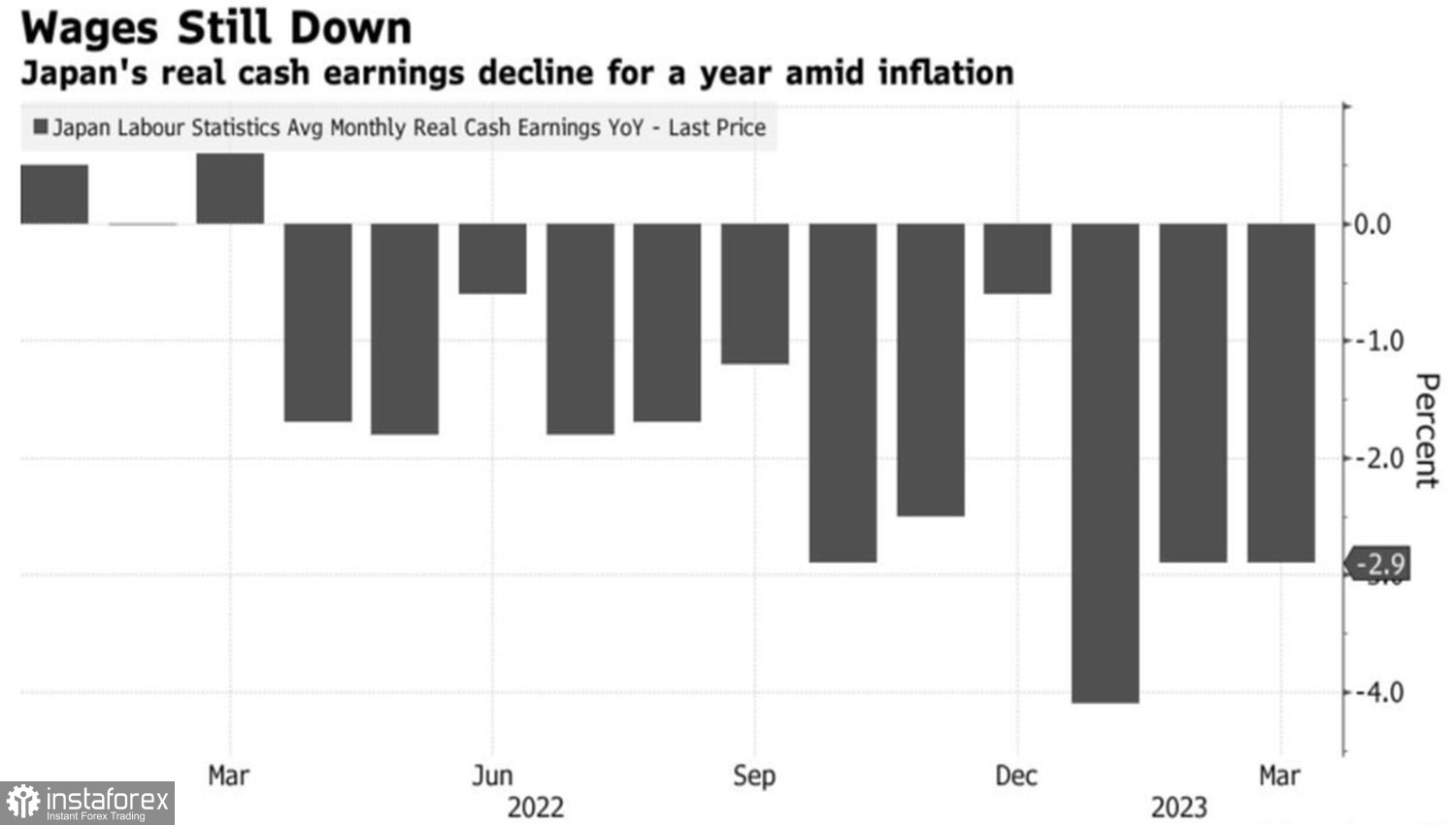

Unfortunately, the decline in real wages for the 12th consecutive month and the sluggish expansion of nominal wages by 0.8% indicate that there is no light at the end of the tunnel. According to the BoJ, the latter indicator should increase by 3% for inflation to stabilize near the 2% target.

Real Wage Dynamics in Japan

Whatever the Bank of Japan is fighting, these are the Bank of Japan's problems. The USD/JPY pair reacts to rumors of monetary policy normalization. If there are none, it may well rise or fall, and these movements will be determined by external factors, primarily the dynamics of U.S. Treasury yields. And there, everything is very confusing.

In theory, the Fed's intention to pause the tightening of monetary policy is a reason to buy U.S. debt securities and reduce their yields. This leads to a weakening of the dollar against the yen. Conversely, strong U.S. labor market statistics contribute to a rally in bond yields and an increase in USD/JPY quotes.

It is not surprising that Jerome Powell's statement that markets may have their own opinion about the "dovish" Fed reversal in 2023 collapsed debt rates and the analyzed pair. Employment growth of 253,000 in April allowed it to find a bottom. However, given the record speculative net shorts on Treasury bonds, USD/JPY movements downward will be faster than upward.

U.S. Bond Speculative Position Dynamics

A decrease in the likelihood of a recession in the U.S. economy and the chances of easing monetary policy by the Fed in July and September lead to increased demand for the U.S. dollar. If the inflation data for April turns out to be better than expected, it will continue to strengthen against major world currencies. And the yen is no exception.

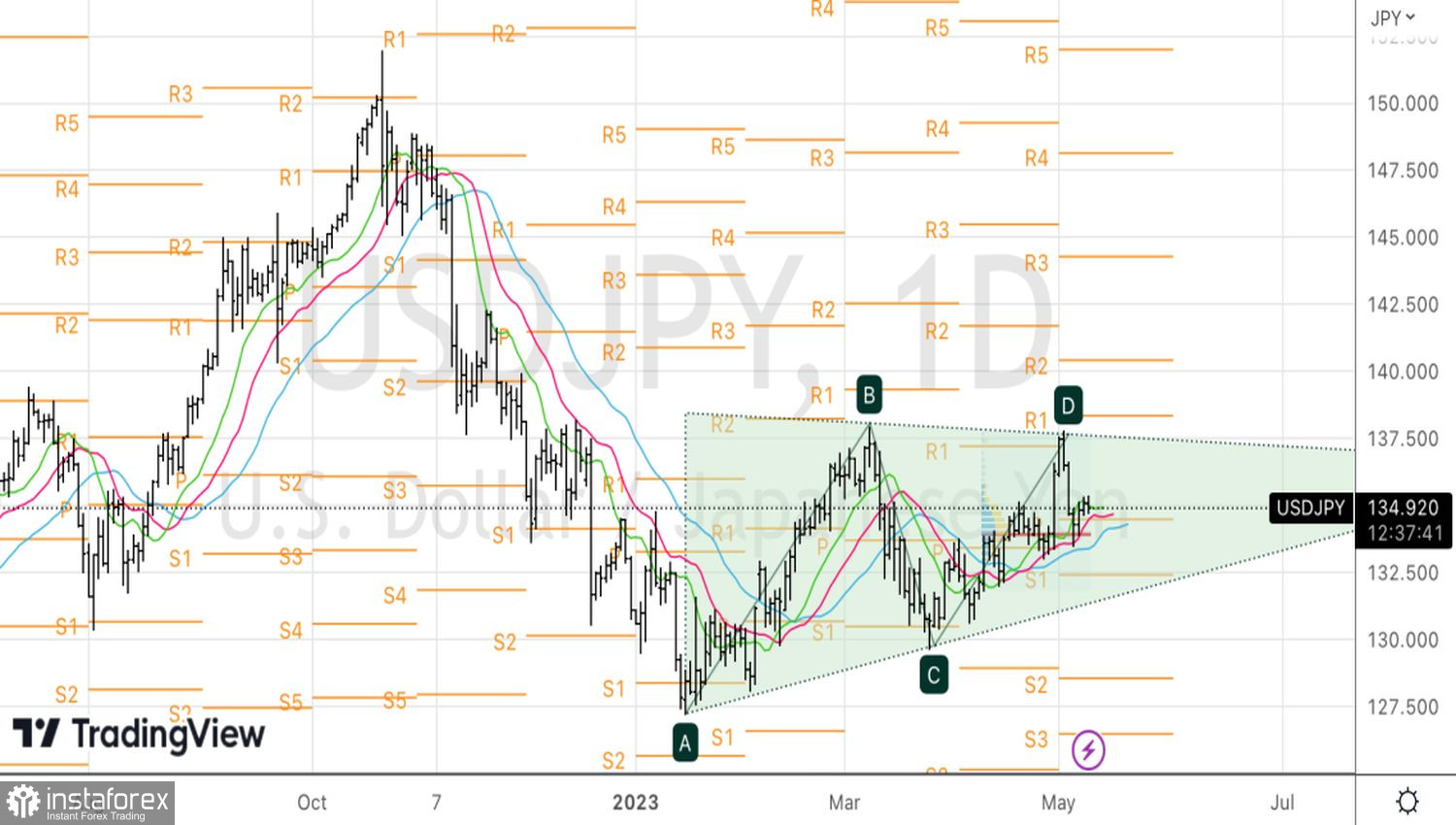

Technically, USD/JPY continues to move within the triangle. Only exiting its boundaries will help the pair choose where to go in the medium term. At the same time, a rebound from the moving averages with a subsequent update of the local low at 135.4 can be the basis for purchases.

Díky analytickým přehledům společnosti InstaForex získáte plné povědomi o tržních trendech! Jako zákazníkovi společnosti InstaForex je Vám k dispozici velký počet bezplatných služeb umožňujících efektivní obchodování.