Stay

Stay

Trading Conditions

Products

Tools

US stock indexes showed solid gains on Wednesday, with the S&P 500 and Dow Jones hitting new all-time highs. The market was positively influenced by the minutes of the latest US Federal Reserve meeting, as well as expectations for September inflation data and the upcoming earnings season of large corporations.

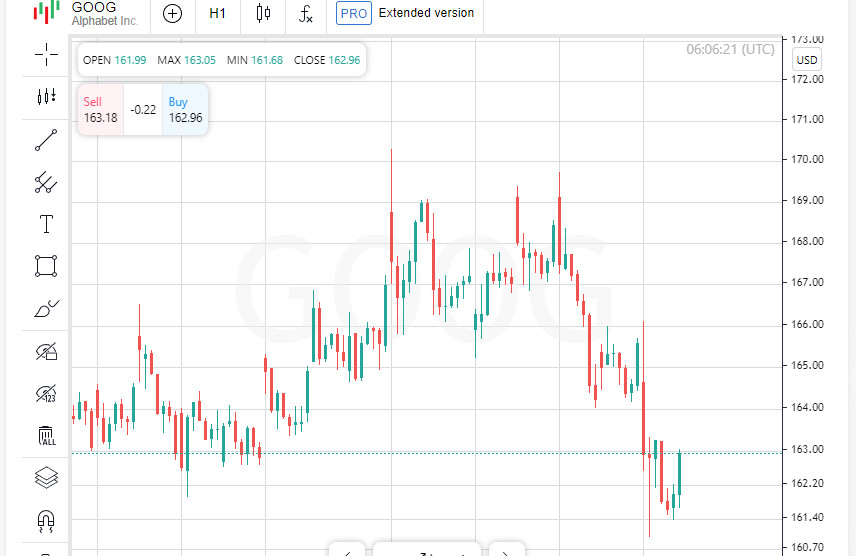

Investor interest focused on shares of tech giant Alphabet, Google's parent company, which showed volatility during the day. The company's shares ended trading down 1.5% after the US Department of Justice announced that it might require the business to be broken up. The agency is considering filing a lawsuit to force the sale of some Google assets, such as the Chrome web browser and the Android operating system, in order to reduce the company's monopoly in the online search industry.

The published minutes of the Fed's September meeting shed light on the discussions among regulators. Most members of the committee supported the idea of cutting the interest rate by 0.5%. However, it was ultimately agreed that such a decision would not mean a commitment to any specific pace of further rate cuts.

According to the FedWatch analytical platform from CME Group, traders currently estimate the probability of a 25 basis point rate cut at 79%. At the same time, the probability that the Fed will decide to keep the current rate level is 21%. This scenario confirms the cautious mood of investors and their expectations regarding the regulator's future actions.

"The minutes confirmed our expectations and calmed the markets. There was discussion of a more aggressive rate cut of 50 basis points, but apparently there was no consensus, and the Fed did not take such a step," commented Lindsay Bell, chief strategist at the investment company 248 Ventures in Charlotte, North Carolina.

The U.S. stock market is anticipating an important macroeconomic event - the publication of inflation data. The consumer price index report, which will be released on Thursday, will attract the attention of traders and analysts, setting the tone for further expectations on monetary policy. In addition, the key stage of the third-quarter earnings season begins on Friday, with leading US banks reporting their first results, which will help determine further market sentiment.

"The Fed minutes showed that the regulator is confident in its strategy, and further inflation developments should not come as a surprise," commented Lindsay Bell, chief strategist at 248 Ventures. Her words reflect market participants' expectations that tomorrow's inflation report will be within the forecast values, without causing sharp movements on the stock exchanges.

This week is marked by increased volatility for the markets. Strong employment data for September, published earlier, forced investors to revise their forecasts for further interest rate cuts. The unexpected growth in the number of jobs was evidence of the resilience of the US economy, dispelling fears of a possible slowdown.

Positive employment news helped fuel optimism among market participants. "There is still a belief in a soft landing scenario, or even no recession, which is supportive for buyers despite the current volatility," Bell said. Investors are hoping that the economy will be able to slow without significant consequences, which will be a positive signal for corporate profits.

Amid the positive mood, the Dow Jones Industrial Average ended the day up 431.63 points, or 1.03%, reaching 42,512.00. The S&P 500 added 40.91 points, which corresponds to an increase of 0.71%, ending the day at 5,792.04. The Nasdaq Composite also showed positive momentum, rising 108.70 points, or 0.60%, to 18,291.62.

Wednesday's close was the S&P 500's 44th record this year, underscoring the market's resilience heading into 2024. The Dow Jones is not far behind, with its previous record close set on October 4. These data suggest that despite macroeconomic uncertainty, stock indices continue to show strong growth.

The U.S. stock market showed positive dynamics in most sectors, with nine out of 11 S&P 500 industry groups ending trading with growth. However, amid macroeconomic-related volatility, interest rate-sensitive utility stocks fell 0.9%. The Telecom Services Index, which includes Alphabet, also fell 0.6%.

"Growing antitrust concerns are causing concern among investors. This could have a significant impact on the entire tech sector, and particularly on its largest players," said Daniel Morris, chief capital markets strategist at BNP Paribas. He stressed that potential lawsuits could limit the market influence of leading tech giants and add uncertainty to their long-term prospects.

Meanwhile, investors were closely monitoring the development of Category 5 Hurricane Milton as it approached the Florida coast. The natural disaster has already brought heavy rains, strong winds, and tornadoes to the region. The threat of further destruction remains high as the hurricane heads toward Tampa Bay and could cause deadly storm surge in coastal areas still reeling from Hurricane Ellen.

Among the major companies under pressure, Boeing stood out. Shares of the aerospace giant fell 3.4% after another round of talks with a key manufacturing union ended inconclusively. The stalled talks heighten uncertainty over the company's future production plans and pose risks to its supply chain.

Amid general volatility in the tech sector, cruise companies unexpectedly posted strong gains. Norwegian Cruise Line increased its market cap by 10.9% after Citi upgraded its rating to "buy." Shares of Carnival followed suit, rising 7% and Royal Caribbean Cruises up 5.2%. The recovery in the tourism sector and investor optimism supported the positive sentiment around these stocks.

Mining company Arcadium Lithium was among the top performers, soaring 30.9% on news that it was acquired by Rio Tinto. The deal will cost $6.7 billion, highlighting Rio Tinto's ambition to strengthen its position in the fast-growing lithium sector, an important raw material for battery production. The deal demonstrates growing interest from major players in resources related to the energy transition and boosts confidence in the industry's prospects.

US-listed shares of Chinese giants Alibaba and PDD Holdings ended the session in the red. Alibaba shares fell 1.6%, while PDD fell 2.3%. The decline was caused by disappointment among investors who expected more active economic stimulus measures from the Chinese authorities. Expectations for new steps to support the slowing economy have not materialized, adding to pessimism over global macro risks.

Despite worries about Chinese companies, the overall picture on U.S. exchanges looked positive. On the New York Stock Exchange, the number of stocks that rose outnumbered those that fell by 1.31 to 1. The session saw 339 new highs and only 49 new lows. The Nasdaq also saw a predominance of bulls, with 2,164 stocks rising against 2,113 falling, for a ratio of 1.02 to 1.

The S&P 500 index showed confident growth, setting 52 new 52-week highs and only two new lows. On the Nasdaq, the picture was less clear, with 88 stocks hitting new highs while 133 posted new yearly lows, reflecting mixed investor sentiment.

US stock markets were muted, with 11.09 billion shares changing hands on the day, below the 20-session average of 12.04 billion. The figure reflects a cautious approach by market participants who are closely monitoring global economic and political cues.

On global markets, the MSCI Index, which tracks stocks around the world, added 0.43%, up 3.61 points to 848.39. It was the second day of gains in a row, indicating that investor sentiment is stabilizing. In Europe, the STOXX 600 Index rose 0.66%, supported by automakers that rebounded from a decline the previous day. Positive data from the European sector gave hope that the region's largest companies are able to cope with the current challenges.

Meanwhile, the Chinese market saw the opposite trend. The Shanghai Composite and CSI300 closed sharply lower, posting their biggest daily decline since February 2020, signaling growing concerns among investors about the future prospects of the world's second-largest economy. The end of the rally in Chinese stocks underscores the fragility of sentiment and uncertainty surrounding Beijing's future actions.

China's General Information Administration has announced that the Finance Ministry is set to unveil fiscal stimulus plans to support the slowing economy on Saturday. Investors are on edge ahead of the press conference, as Beijing's new measures will determine the future trajectory of the country's economic growth, which has been struggling in recent weeks amid weakening domestic demand and an unstable external environment.

US Treasury yields rose after the Federal Reserve minutes and comments from Dallas Fed President Laurie Logan. The dynamics were also influenced by a successful auction of 10-year notes. The yield on the benchmark bond rose by 3.8 basis points to 4.073%, indicating growing expectations for rate hikes in the future. Meanwhile, the yield on the 2-year Treasury note, which is more sensitive to short-term rates, rose by 4.3 basis points to 4.022%.

Earlier this week, the yield on the 10-year Treasury note broke the psychological barrier of 4% for the first time in two months. This level is considered by analysts as an important indicator of the state of the credit market, which has increased concerns about the sustainability of US economic growth. Higher yields could also put pressure on borrowing costs for businesses and consumers.

The US dollar strengthened against major global currencies amid rising bond yields. The dollar index, which tracks the dollar against a basket of six currencies, rose 0.42% to 102.92 points. At the same time, the euro fell 0.38% to $1.0938. The dollar also strengthened significantly against the Japanese yen, rising 0.76% to 149.32 yen per dollar, reflecting growing investor expectations for a tightening of monetary policy in the US.

By contrast, the pound sterling weakened, falling 0.34% to $1.3059 amid ongoing uncertainty over the UK's economic outlook and possible moves by the Bank of England. Investors are cautious about the British currency, awaiting further data on inflation and activity in the services sector.

Oil prices continue to fall for the second session in a row, despite geopolitical risks and potential supply disruptions. The main factor behind the decline is the growth of oil inventories in the US, which has raised concerns about oversupply. The cost of American WTI crude oil fell by 0.45% to $73.24 per barrel. Brent futures also ended the day in the red, falling by 0.78% to $76.58 per barrel.

However, the decline in quotes was limited by the threat of supply disruptions due to tensions in the Middle East and the aftermath of Hurricane Milton, raging in the United States. Potential disruptions to energy production and transportation are keeping prices from falling more sharply, supporting market sentiment as participants await further signals about the state of supply in the global oil market.

InstaForex analytical reviews will make you fully aware of market trends! Being an InstaForex client, you are provided with a large number of free services for efficient trading.