Stay

Stay

Trading Conditions

Products

Tools

The S&P 500 and Nasdaq both hit new record closing highs on Monday, despite investor caution ahead of consumer price data and the Federal Reserve's policy announcement this week.

Nvidia (NVDA.O) shares provided some support to the Nasdaq and S&P 500, rising 0.7% after a 10-for-one stock split. Some investors now believe the chipmaker could be added to the Dow.

The May CPI report is due Wednesday, coinciding with the end of the Fed's two-day meeting.

The central bank is expected to leave interest rates unchanged while issuing updated economic and policy forecasts. Investors will be watching closely for any hints of a possible rate cut down the road.

"It's a big week for the market in terms of Fed commentary and statements," said Quincy Crosby, chief global strategist at LPL Financial in Charlotte, North Carolina.

"Additionally, the CPI report is due Wednesday morning. Everything related to the economy and inflation is viewed through the prism of the Fed's actions by the market," he added.

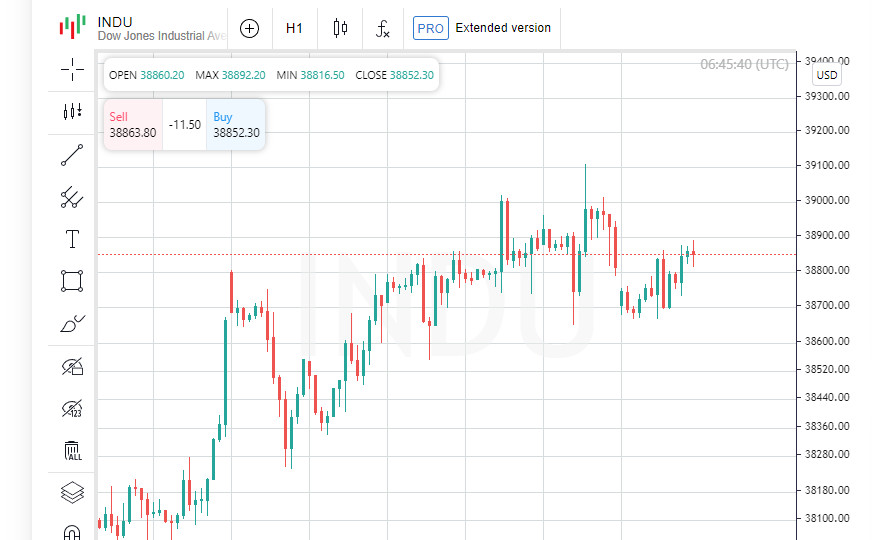

The Dow Jones Industrial Average (.DJI) rose 69.05 points, or 0.18%, to 38,868.04. The S&P 500 (.SPX) rose 13.8 points, or 0.26%, to 5,360.79, and the Nasdaq Composite (.IXIC) added 59.40 points, or 0.35%, to 17,192.53.

Traders trimmed their expectations for a September rate cut after stronger-than-expected May employment data on Friday, leaving the chance of a cut at 50%.

Apple (AAPL.O) shares fell 1.9% on the first day of its annual iPhone developer conference, with investors eagerly awaiting news on how the company will integrate artificial intelligence into its products.

Among the day's best performers were Southwest Airlines (LUV.N), which jumped 7% after activist investor Elliott Investment Management acquired a $1.9 billion stake in the company.

Diamond Offshore Drilling (DO.N) rose 10.9% after oilfield services company Noble (NE.N) announced it was buying a rival for $1.59 billion. Noble also rose 6.1%.

Advancing stocks outnumbered declining stocks 1.06-to-1 on the New York Stock Exchange, while gainers were outnumbered 1.01-to-1 on the Nasdaq.

The S&P 500 posted 19 new 52-week highs and five new lows, while the Nasdaq Composite posted 56 new highs and 177 new lows.

Trading volume on U.S. exchanges totaled 10.39 billion shares, below the 20-day average of 12.80 billion.

MSCI's global share index rose on Monday, despite investor expectations for key U.S. inflation data and an upcoming central bank meeting. The euro, however, slipped after French President Emmanuel Macron announced an early election.

U.S. Treasury yields rose as investors digested Friday's labor market data and looked ahead to consumer price data and a Federal Reserve statement this week. Eyes were also focused on the Bank of Japan's possible decisions.

Adding to the uncertainty was political instability in the euro zone's second-largest economy. Far-right gains in the European Parliament elections on Sunday prompted Macron to call a national election.

The euro hit a one-month low against the dollar, while European stocks also suffered.

"The uncertainty is coming from multiple sources. "The European elections over the weekend added volatility to the markets," said Chad Oviatt, director of investment management at Huntington National Bank.

The STOXX 600 index, which covers pan-European stocks, closed down 0.27%. France's blue-chip CAC 40 index fell 1.4%, hitting a more than three-month low.

However, the MSCI Global Equity Index (.MIWD00000PUS) turned from bearish to bullish territory by the end of the day, and Wall Street partially recouped its gains. As a result, the global index rose 0.75 points, or 0.09%, to 794.99.

Huntington National Bank's Oviatt said investors are eagerly awaiting the release of U.S. consumer price index (CPI) inflation data on Wednesday morning, ahead of the Federal Reserve's policy decision Wednesday afternoon.

Adding to the uncertainty about the impact of economic data on the Fed's interest rate policy was Friday's jobs report, which showed the U.S. economy added significantly more jobs in May than expected and annual wage growth accelerated again.

"Everyone seems to be hoping for a rate cut, but so far that hasn't been the case. "So everyone is looking to the CPI data on Wednesday morning, hoping that will give us more information and commentary from the Fed in the afternoon to clarify the situation," said Jim Barnes, director of bonds at Bryn Mawr Trust in Berwyn, Pennsylvania.

U.S. Treasury yields, which move inversely to prices, rose Monday, reflecting expectations for higher, longer-term U.S. rates.

The benchmark 10-year Treasury yield rose 4.1 basis points to 4.469%, up from 4.428% late Friday. The 30-year yield also rose, up 4.8 basis points to 4.5958%.

The 2-year yield, which typically responds to changes in interest rate expectations, rose 1.5 basis points to 4.8846% from 4.87% late Friday.

In the foreign exchange market, the euro fell to its lowest since May 9 against the U.S. dollar, down 0.37% to $1.076. Earlier, the euro hit a near two-year low against sterling.

The dollar index, which measures the greenback against a basket of currencies including the euro and the Japanese yen, rose 0.08% to 105.14. Against the Japanese yen, the dollar strengthened 0.21% to 157.03.

The Bank of Japan (BOJ) is holding a two-day monetary policy meeting this week and may offer new guidance on tapering its massive bond purchases.

In commodities, oil prices hit a one-week high on hopes for a pickup in fuel demand this summer. However, a stronger dollar and fading expectations for a U.S. rate cut capped gains.

U.S. crude rose 2.93% to $77.74 a barrel, while Brent crude rose 2.52% to $81.63 a barrel.

Gold prices pared their losses after their biggest drop in 3.5 years in the previous session, as investors awaited inflation data and a policy statement from the Federal Reserve.

Spot gold rose 0.72% to $2,309.15 an ounce.

InstaForex analytical reviews will make you fully aware of market trends! Being an InstaForex client, you are provided with a large number of free services for efficient trading.