Stay

Stay

Trading Conditions

Products

Tools

US stock markets ended trading on Thursday with a confident rise, helped by the Federal Reserve's decision to cut interest rates by a quarter of a percentage point (25 bps). This development strengthened the positive trend that began after Donald Trump returned to the US presidency.

The Federal Reserve has decided to cut rates by 0.25%, citing signs of weakness in the labor market and a gradual move in inflation toward the central bank's 2% target.

Markets had largely expected the move, almost entirely factoring the rate cut into their forecasts for the November meeting. Investors are now watching closely for any follow-up comments from Fed officials that could shed light on the future direction of monetary policy.

Expectations of a return to corporate tax cuts and Trump-led regulatory easing have fueled investor optimism, sending key stock indexes higher. The Dow Industrials and S&P 500 posted their biggest one-day gains in two years last trading session, while the Nasdaq was not far behind, continuing to move in the green.

"The Fed has kept the drama out of this eventful period," said Brian Jacobsen, chief economist at Annex Wealth Management in Wisconsin. "A quarter-percentage point cut leaves the federal funds rate still in cap territory, but it's not as tight as it used to be." He said Trump's return to the presidency could bring a modest improvement in growth, but it would also likely lead to higher inflation. "The Fed will likely have to cut rates at a more cautious pace," Jacobsen concluded.

The Dow Jones Industrial Average (.DJI) was virtually unchanged, down just 0.59 points to 43,729.34. The S&P 500 (.SPX) added 0.74%, rising 44.06 points to 5,973.10, while the tech-heavy Nasdaq Composite (.IXIC) was the biggest gainer, rising 1.51%, or 285.99 points, to end the session at 19,269.46.

Communications (.SPLRCL) was the biggest gainer among sectors, jumping 1.92%. This was helped by a massive 11.81% gain in Warner Bros Discovery (WBD.O) after the company reported unexpectedly strong third-quarter earnings, which encouraged investors to buy into the sector.

The financial sector (.SPSY) was among the laggards, losing 1.62% after a strong rally in the previous session. In particular, banks (.SPXBK) fell 3.09%, reversing a significant gain from Wednesday. JP Morgan (JPM.N) and Goldman Sachs (GS.N) also showed negative dynamics, with their shares falling 4.32% and 2.32%, respectively, putting pressure on the Dow.

Sentiment towards further rate cuts has become less optimistic in recent weeks. Economic data points to economic resilience, which could push inflation higher. Such a scenario is likely amid expected tariff changes and increased government spending under the policies of the new Trump administration.

Fed Chairman Jerome Powell noted that the final decision on the central bank's December policy has not yet been made. However, he stressed that the Fed is prepared to adjust the course and pace of its actions given the current economic uncertainty.

One of the key factors attracting investors' attention remains the possibility of the Republicans taking control of both houses of Congress. If this happens, it will be easier for Donald Trump to advance his economic agenda, which will potentially increase support for the business sector and cause a positive reaction in the market.

After a wild rally in recent weeks, 10-year Treasury yields retreated for a time. The benchmark yield, which hit a four-month high of 4.479% on Wednesday, eased slightly after the Fed's announcement to close at 4.332%.

U.S. jobless claims rose slightly last week, data showed Thursday, pointing to stable labor market conditions. The lack of a significant increase in unemployment is a boost to confidence in economic resilience, easing concerns about the need for urgent changes in monetary policy. NYSE and Nasdaq rally, S&P 500 and Nasdaq Composite hit record highs

On the New York Stock Exchange, gainers outnumbered losers by nearly twice (1.94 to 1). On the Nasdaq, the ratio was 1.18 to 1. The S&P 500 posted 56 new 52-week highs and just 4 new lows, while the Nasdaq Composite posted 193 new highs and 88 new lows.

Turnover on U.S. exchanges reached 16.78 billion shares on Thursday, well above the average daily volume of 12.46 billion shares over the past 20 trading days.

The MSCI Index of global equities (.MIWD00000PUS) rose 0.9% to a new record high, signaling continued appetite for global markets amid a pickup in economic activity.

Europe's STOXX 600 Index (.STOXX) rose 0.6% following a strong start to Asian trading. The index was also supported by Chinese blue chips, which jumped 3% (.CSI300). Investor sentiment was boosted by expectations of more stimulus measures, which outweighed concerns over escalating trade tensions.

"Equities are reflecting expectations of lower corporate taxes and reacting positively to the prospect of deregulation, which will benefit earnings," said Naomi Fink, chief strategist at Nikko Asset Management. Companies across industries see new growth potential in the policy, spurring further investor interest in key assets.

U.S. Treasury yields continue to decline following the Fed's rate cut, although analysts warn that the process may be less sustainable than expected under the new Trump administration.

There is growing consensus among economists that a Republican election win could be a catalyst for more accommodative fiscal policy. Matthias Scheiber, head of portfolio management at Allspring Global Investments, believes that the combined effect of new tariffs and stimulus could boost the economy but also increase inflation pressures.

The yield on the 10-year Treasury note fell 9 basis points to 4.3355% on Thursday, after rising 14 basis points the previous day. The 30-year yield also fell more than 6 basis points to 4.5393% after a big jump the previous day.

The dollar fell 0.7% against a basket of major currencies, reversing Wednesday's biggest one-day gain in more than two years. Many traders began to close positions on a Trump victory and were looking ahead to the Fed's upcoming decision, weighing on market sentiment.

The euro rose 0.7% to $1.0803, partly reversing a 1.8% average loss the previous day. The euro is recovering as investors digest the latest political developments in Germany, where Chancellor Olaf Scholz fired Finance Minister Christian Lindner, leading to the collapse of the coalition government and likely to lead to early elections. Euro Strengthening Forecasts

Deutsche Bank analysts note that while events in Germany are still in the early stages, potential political stability could strengthen confidence in the euro. Economic forecasts also point to possible positive effects if the new government adopts a more proactive fiscal stance.

German 10-year bond yields rose 4.8 basis points to 2.441%, reflecting market expectations for future EU policy developments.

Meanwhile, the Bank of England has cut interest rates by a quarter of a percentage point, its second such move since 2020. The regulator has signaled that further cuts will be gradual, given the risks of rising inflation following the new government's budget presented last week.

The British pound also regained some of its positions and rose by 0.8%, rising to $1.2986 after falling by 1.24% on Wednesday.

Norway and Sweden central banks held their meetings on Thursday, which resulted in no significant changes for the currency markets, fully meeting analysts' expectations. Norges Bank decided to leave interest rates at a 16-year high, maintaining its commitment to tight monetary policy. At the same time, Sweden's Riksbank cut rates by 50 basis points, softening its approach to monetary policy.

The Bitcoin cryptocurrency has rapidly recovered its recent losses and reached a new all-time high of $76,780 overnight. Against this backdrop, Donald Trump said that he would make the United States the "crypto capital of the world," which has increased investor interest in digital assets.

After a significant drop of more than 3% on Wednesday, gold showed confident growth, increasing by 1.8% and reaching $2,707.21 per ounce. Despite this, the price of gold remains close to its recent record high of $2,790.15.

Oil prices also showed positive dynamics after the sell-off caused by the US presidential election. Brent crude futures rose 0.6% to $75.40 a barrel, while U.S. WTI crude rose 0.5% to $72.04 a barrel.

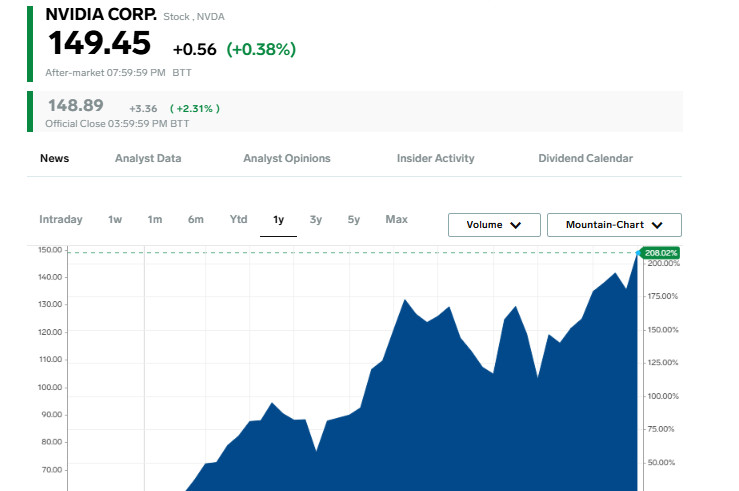

The leading AI chipmaker rose 2.2%, helped by investor optimism that regulation and tax cuts will be eased following the Republican nominee's election victory. Nvidia's market capitalization reached $3.65 trillion, surpassing Apple's record high of Oct. 21 and becoming the world's most valuable company, according to LSEG.

Apple shares gained 2.1% on Thursday, taking the company's market capitalization to $3.44 trillion. The gains are part of a broader trend in tech, with the S&P 500 index of major tech companies gaining more than 4% over the past two days as Donald Trump wins the presidential election.

Nvidia has been the biggest beneficiary of the recent AI frenzy, outperforming giants like Microsoft and Alphabet. Nvidia shares have risen 12% in November and have tripled in value this year. Nvidia is steadily outperforming the world's biggest companies in the race to dominate computing power and cutting-edge technology.

Today, Nvidia's market cap exceeds the combined value of giants like Eli Lilly, Walmart, JPMorgan, Visa, UnitedHealth Group, and Netflix. Analysts forecast Nvidia's quarterly revenue to increase 80% to $32.9 billion when the company reports results on November 20, underscoring its growing influence in the global market.

In June, Nvidia temporarily became the world's most valuable company, but was later overtaken by Microsoft and Apple. Today, the three tech giants are locked in a tight race for the top spot, with each remaining at similar market caps.

InstaForex analytical reviews will make you fully aware of market trends! Being an InstaForex client, you are provided with a large number of free services for efficient trading.