Maradok

Maradok

Kereskedési feltételek

Products

Eszkozok

To be honest, The Fed's decision yesterday put everything in its place, as well as explained what has happened over the past few days. However, its actions put other central banks in an extremely uncomfortable position, especially the European Central Bank, who was completely pinned against the wall.

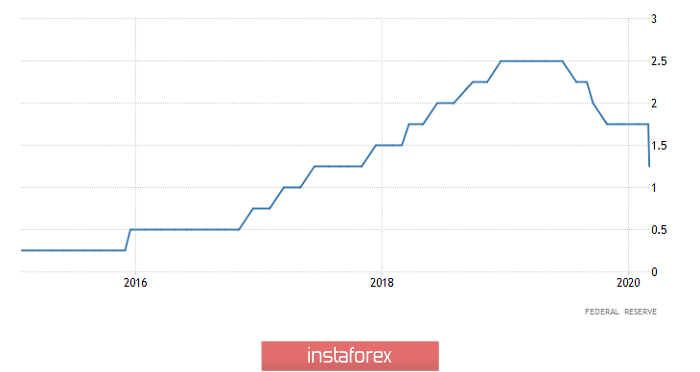

The decision to reduce the interest rate from 1.75% to 1.25% two weeks before the scheduled meeting of the Fed was extremely strange. However, the high risks that the coronavirus carries justifies it. Allegedly, even though the damage is not clear yet, the virus can cause serious damage to the economy. Back in 2008, the Federal Reserve also held an unscheduled meeting in the same way and lowered the refinancing rate. It happened during a raging financial crisis, where the panic in the markets affected not just the economic growth, but also ordinary people.

The official comment on yesterday's decision began with the statement saying that the US economy is in excellent condition. It was followed by a small remark about the coronavirus and its possible risks, justifying that the decision is designed to maintain an incredibly high level of employment, perhaps the highest in history, as well as price stability. To be honest, the Fed's decision, as well as the market's reaction to it, put a lot of things in their place. Since the dollar has already declined, it has nowhere else to go. In my opinion, someone already knew about the unexpected decision of the Fed, as the market was moved with large volumes. In addition, the media has already discussed the possibility of the major central banks reducing their interest rates for the sake of reinsurance due to the coronavirus. It just never occurred to anyone that it could happen like this, or that the decline will be immediately so large-scale.

The interest rate (United States):

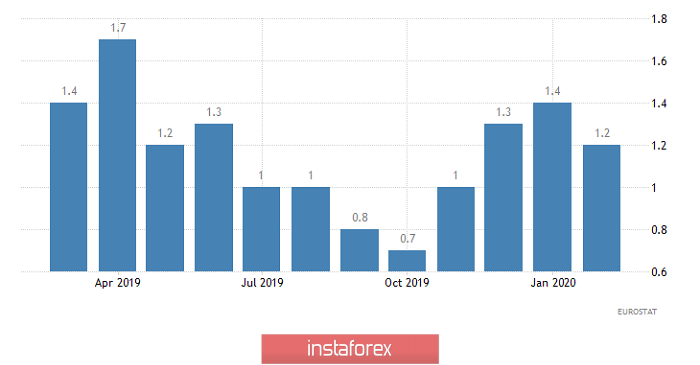

The market did not react to the preliminary data on inflation in Europe, even though it declined from 1.4% to 1.2%. Such a serious reduction in inflation without any decisions from the Fed immediately suggests that Christine Lagarde should revise the current monetary policy of the European Central Bank. Nevertheless, the decline in producer prices in Europe from -0.6% to -0.5% indicates that improvement is still present. In addition, the unemployment rate in Europe remained unchanged, just like in Italy, although the unemployment rate in Italy was expected to fall from 9.8% to 9.7%. In Spain, the number of unemployed fell by 7.8 thousand, instead of increasing by 2.0 thousand. However, against the background of what is happening, all this fades. Nevertheless, you should pay attention to the yield of Spanish bills that were placed yesterday, where the yield of 6-month bills decreased from -0.476% to -0.509%, and the yield on 12-month bills fell from -0.454% to -0.497%. This is another example of the constant decline in the yield of European debt securities, which indicates the possibility that the ECB will reduce its interest rate.

Inflation (Europe):

In contrast with the euro, the growth of the pound was quite noticeable. It is justified by the data on the index of business activity in the construction sector, which rose from 48.4 to 52.6. It was predicted to grow to only 48.6.

Index of business activity in the construction sector (UK):

The question now is not how much the dollar can fall in price, but what the other central banks will do regarding the situation. The Fed's actions put everyone at an extreme disadvantage, as the scale and influence of the system cannot be ignored. We need to take some steps, and there is only one solution - reduce your own interest rates. Now, the main question is: when will the European Central Bank reduce its interest rate to a negative value? Will this happen on March 12, during the scheduled board meeting? Or will Christine Lagarde decide to hold an extra-curricular emergency meeting? What will happen to the announced plans to revise the monetary policy? Has something fundamentally changed? Will the decision of the Fed lead to a change in the trend of the dollar, which has been going on since 2009? This is highly unlikely though, because other central banks will now have to lower their interest rates, following in the wake of the Federal Reserve System. In addition, the real macroeconomic situation has not disappeared, and it is quite impossible to change it immediately. The dynamic clearly favors the dollar, so as soon as the ECB and BOE reduce their interest rates, a reversal movement will be seen, and the dollar will resume its usual pattern of strengthening.

In the current situation, or at least for a couple of days, no macroeconomic statistics will worry anyone. We should not forget about it though, as it determines the trend. Anyhow, a number of encouraging data has been released in Europe. The growth rate of retail sales in Germany accelerated from 1.7% to 1.8%, although they predicted a slowdown to 1.4%. Based on this, they forecasted the retail sales in Europe to grow from 1.3% to 1.4%. Today, sales data can really please and even temporarily contribute to the growth of the euro. The index of business activity in the Italian services sector rose from 51.4 to 52.1, which was better than forecasts showing a decline to 51.9. In Spain, the index of business activity in the service sector fell from 52.3 to 52.1, even though it should have grown to 52.7. In France, everything is pretty good, as the index of business activity in the service sector rose from 51.0 to 52.5. Most importantly, the composite PMI rose from 51.1 to 52.0 instead of 51.9. In Germany though, which is the engine of the European economy, things are somewhat different. The index of business activity in the service sector fell from 54.2 to 52.5, and the composite index declined from 51.2 to 50.7. Nevertheless, the pan-European indicators did not suffer much from this, as the index of business activity in the service sector increased from 52.5 to 52.6, and the composite index rose from 51.3 to 51.6. However, the GDP in Italy showed a slowdown from 0.5% to 0.1%. A recession doesn't seem like such a fantastic idea, but much will depend on pan-European retail sales data, which is currently not looking good, not only because of the growth in Germany, but also in the possible acceleration of the retail sales in France from 2.5% to 3.2%.

Retail sales (Europe):

The pound does not have any hopes for growth at all, as the index of business activity in the service sector should fall from 53.9 to 53.3. The composite index should also remain unchanged. Now that everyone is well aware that the next meeting of the Bank of England's Board will decide to reduce the refinancing rate, the only question is: will it be up to 0.50% or 0.25%?

Composite index of business activity (UK):

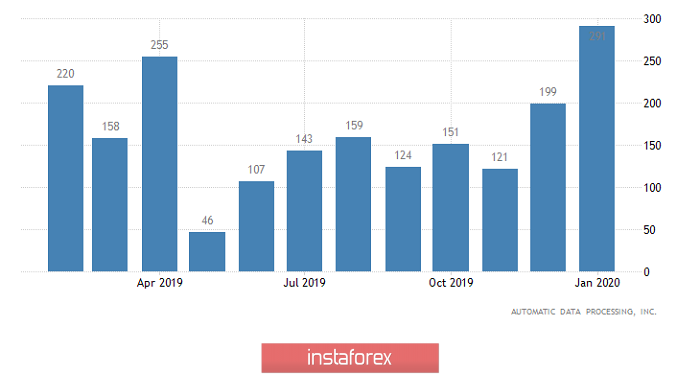

The growth of the dollar will be restrained by the US macroeconomic data. The most important indicator is the change in employment from ADP, which should grow by 175 thousand, against 291 thousand in the previous month. The index of business activity in the service sector should fall from 53.4 to 49.4, so as a result, the composite PMI should fall from 53.3 to 49.6. The worst case scenario is that both indexes will fall below the 50-point mark, which separates growth from stagnation. Let me remind you that the next report of the US Department of Labor will be published on Friday.

Change in employment (United States):

Today, the euro will hang around 1.1150-1.1200, and will gravitate closer to the upper border. The next term is the mark in the line of 1.1100.

Due to weak macroeconomic statistics, the pound will continue to decline. The nearest benchmark is 1.2750, while the next mark is 1.2700.

InstaForex analytical reviews will make you fully aware of market trends! Being an InstaForex client, you are provided with a large number of free services for efficient trading.