Maradok

Maradok

Kereskedési feltételek

Products

Eszkozok

The pandemic is back, and this is clearly not to the liking of the oil market. The rise in the number of COVID-19 cases in Britain to record highs, a sharp increase in hospitalizations in the United States, and a nationwide lockdown in the Netherlands raise doubts about the IEA's forecast that Omicron will not reverse the recovery in global demand for black gold but will only slow down this process. Humanity hopes that the new strain is not as dangerous as the previous ones, but the oil market is giving alarming signals.

Even though ECB President Christine Lagarde, following the results of the December meeting of the ECB, optimistically stated that each subsequent version of COVID-19 will have less and less impact on the economy, Omicron is taking over Europe.

In the U.S., the percentage of detected infections since Omicron exceeds 70%, which, coupled with the reluctance of individual Democratic senators to vote for a new $1.75 trillion stimulus package from President Joe Biden, increases fears of a slowdown in GDP and contributes to a correction in stock indices. Global risk appetite is falling, dragging Brent and WTI into the quagmire.

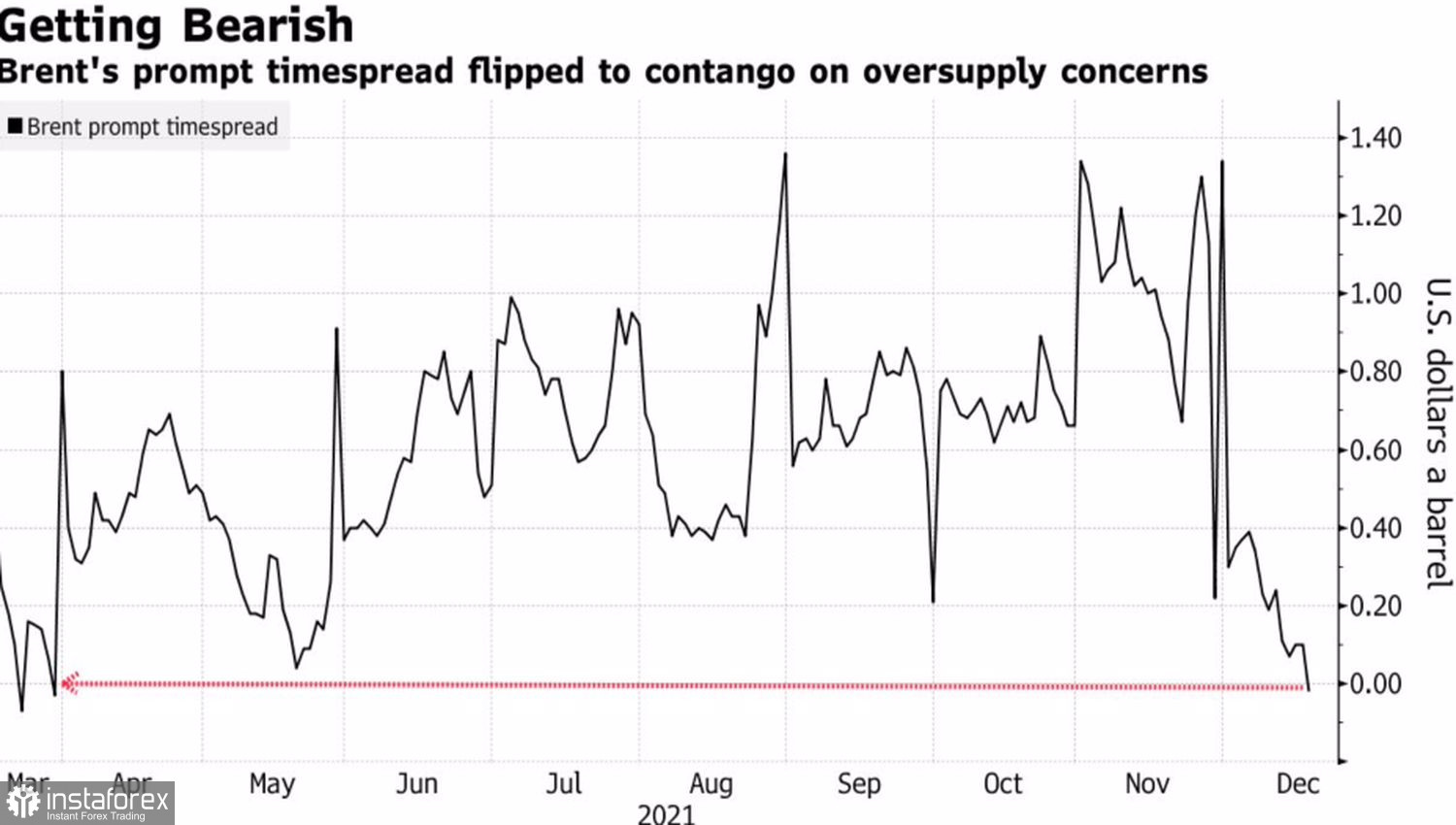

The structure of the oil market is becoming bearish. It indicates an oversupply, although demand dominated from March to December.

Oil market structure

The increase in production was due to the rise in gas prices. If earlier the energy crisis led to a parallel increase in its value and quotes of Brent and WTI on fears that expensive blue fuel will be replaced by oil, now the views of investors have changed. They perceive the cold winter and Russia's reluctance to increase gas supplies as a sure sign that the supply of oil will grow, which will negatively affect prices. Even the activity of OPEC+ does not help.

According to Reuters, the level of fulfillment of obligations to reduce production by the Alliance in November was 117%, in October 116%. Production remains below target levels, but this fact has not helped either the Texas or North Sea variety so far.

The pressure on oil is exerted by the confident U.S. dollar. The Fed's intention to get rid of the quantitative easing program as soon as possible, ending it in March, and not in June, as previously planned; FOMC forecasts of a federal funds rate hike at three meetings of the Open Market Committee; as well as Christopher Waller's statement that monetary policy tightening may occur as early as March, allow the U.S. currency boost its confidence. Oil is quoted in U.S. dollars, so a rally in the USD index is usually a negative factor for Brent and WTI.

The Fed's monetary restrictions, the proliferation of Omicron, and the failure of Biden's new fiscal stimulus bill to get through Congress are allowing large banks and investment firms to cut their forecasts for U.S. economic growth. Specifically, Goldman Sachs cut estimates of GDP expansion from 3% to 2% in the first quarter, from 3.5% to 3% in the second, and from 3% to 2.75% in the third.

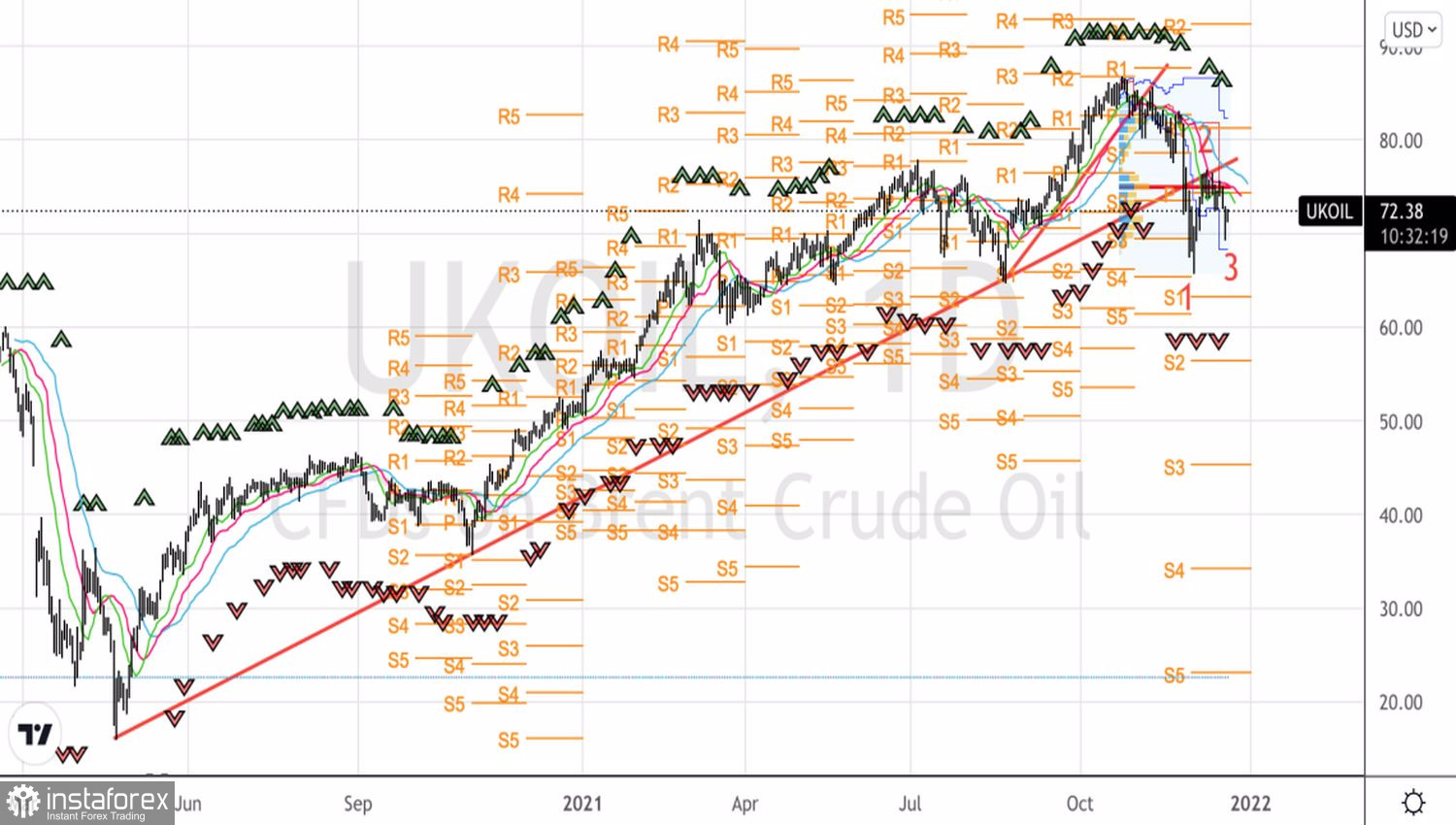

Technically, only the return of Brent to the fair value of $75.25 per barrel will allow a return to the idea of forming longs.

Brent, Daily chart

InstaForex analytical reviews will make you fully aware of market trends! Being an InstaForex client, you are provided with a large number of free services for efficient trading.