Zostať

Zostať

Podmienky obchodovania

Nástroje

The U.S. Bureau of Labor Statistics reported Tuesday that the country's annual inflation rate fell to 7.1% in November from 7.7% in October, which was also below the 7.3% forecast. The annual core CPI, which excludes volatile food and energy prices, fell to 6% (down from 6.3% in October and a forecast of 6.1%). The data suggest that the Fed's efforts to rein in inflation are showing some results.

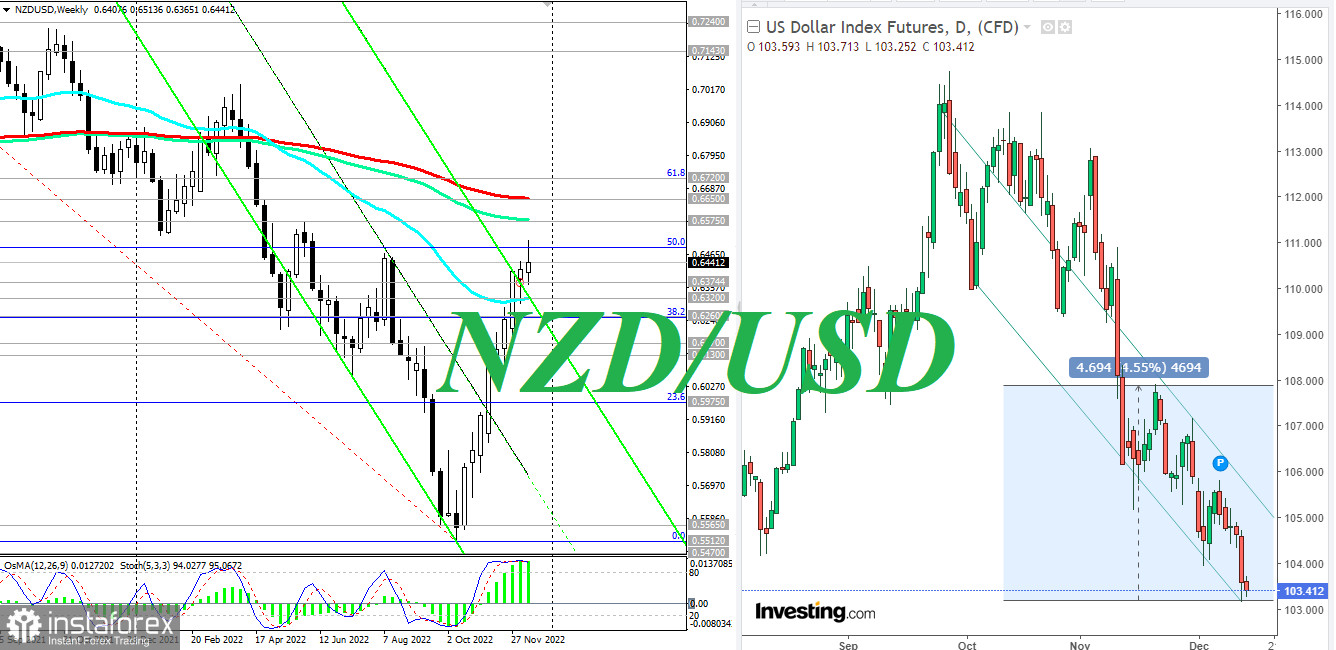

According to many observers, the issue of the Fed's interest rate hike at the December meeting (which ends today at 19:00 GMT) at 0.50% (rather than 0.75%, as it was in June, July, September and November) is a done deal. Meanwhile, the Fed Funds final rate forecast was lowered from 4.98% to 5.0% to 4.86% after the aforementioned report. Yesterday, the dollar index (DXY) plummeted 1.3%, breaking through 104.00 and falling to 103.15, then recovering somewhat by the end of the trading day.

Today, the dollar and the dollar index remain under pressure, and DXY futures are currently trading near 103.41, 26 points above yesterday's local (since July) low.

Many economists are already predicting the Fed will cut the size of the rate hike again in early 2023, moving to 0.25% hikes in February and March.

But what will happen if the Fed does not meet the expectations of dollar sellers and raises the interest rate by 0.75%, against market expectations, and Fed Chairman Jerome Powell makes hawkish statements at a press conference following this meeting? One way or another, inflation in the U.S. remains unacceptably high (the Fed's annual inflation target is 2%). Powell may recall this again, also warning market participants that a premature end to the fight against inflation may be more serious than a belated one.

A steady return of inflation to 2% is still far away. Services sector inflation, for example, rose in November above expectations, and the overall core CPI over the past three months increased by 4.3% YoY. At the same time, the growth rate of wages is about 5%, which will continue to contribute, if not to growth, then to a high level of inflation. This will deter the Fed from possibly hasty steps to curtail the super-tight cycle in the inflation-fighting mode.

If Powell fails to dissuade the sellers of the dollar, and his "hawkish" comments will be more like just attempts to slow down the accelerated weakening of the U.S. currency, then a further fall in the dollar cannot be avoided.

A breakdown of the 103.00 level will send the DXY index (CFD #USDX in the MT4 trading terminal) first to the May low of 101.30, and then to the psychologically significant mark of 100.00.

Thus, the focus of today is the publication (at 19:00 GMT) of the Fed's rate decision and press conference at 19:30.

Tomorrow, market participants will evaluate the results of the meetings of the Swiss National Bank, the Bank of England and the European Central Bank. Meanwhile, today's economic calendar will be closed by the publication (at 21:45 GMT) of Statistics New Zealand's Q3 GDP report. This report reflects the overall economic indicators and has a significant impact on the decision of the Reserve Bank of New Zealand on monetary policy issues. The indicator is expected to grow by +0.9% (+5.5% YoY) after the previous values at +0,4%, +1,2%, +3,1%, -0,2%, +2,9%, -0,8%, +0,2%, -11,3%, 0%, +1,7%.

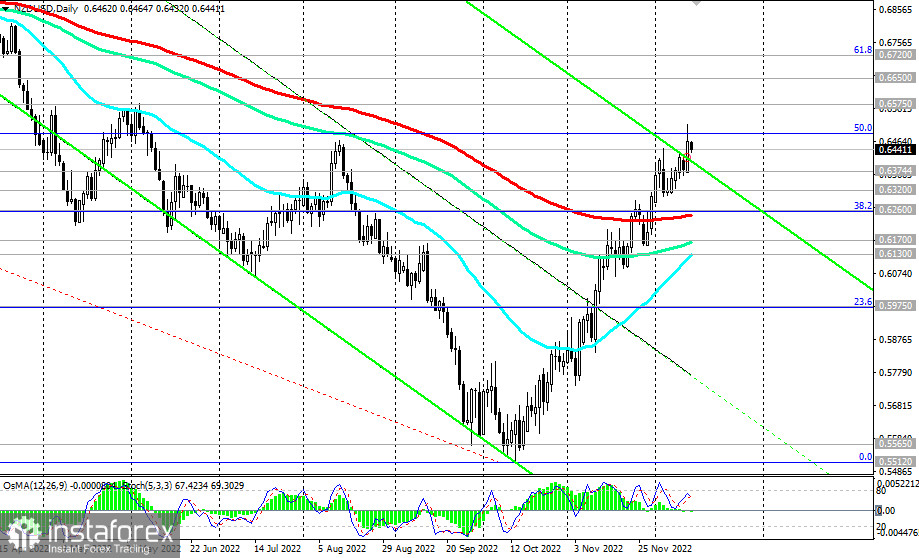

This is a fairly solid increase in the New Zealand GDP. Its growth means an improvement in economic conditions, which makes it possible (with a corresponding increase in inflation) to tighten monetary policy, which, in turn, usually has a positive effect on the quotes of the national currency. Therefore, when the forecast is confirmed, it is logical to assume the strengthening of NZD, including in the NZD/USD pair, which, as of writing, is trading near 0.6440, maintaining positive dynamics in corrective growth towards key resistance levels 0.6675, 0.6650.

InstaForex analytical reviews will make you fully aware of market trends! Being an InstaForex client, you are provided with a large number of free services for efficient trading.