Zostať

Zostať

Podmienky obchodovania

Nástroje

US stock indexes have advanced slightly and are ready to extend Friday's rally. At the end of last week, several Fed policymakers presented arguments in favor of easing the regulator's rate hike policy, which contrasted with hawkish statements by EU officials.

Concerns about the US economy, which is widely expected to fall into recession at the end of 2023, the ongoing debate in Congress over the debt ceiling and signals from US companies during the fourth-quarter earnings season are all impacting sentiment regarding the US stock market. Before the opening bell, S&P 500 and Nasdaq futures edged up by only 0.2%, while Dow Jones futures were unchanged.

In the EU, the Stoxx 600 remained quite stable despite hawkish statements by ECB policymakers. Last week, Klaas Knot, the president of the Dutch central bank, made the case for continued ECB policy tightening, arguing that core inflation was still rising despite the core CPI slowing down. Over the weekend, Klass Knot reiterated his statements, saying that rates would be raised both in May and June, without specifying the size of the hikes.

The euro surged to its highest level since April 2022 as a result. The European currency rose by nearly 2% against the US dollar this year after falling nearly 6% last year.

As noted above, markets followed recent comments from Fed officials on Friday, particularly those by Fed Governor Christopher Waller, who said that future policy appeared restrictive enough and supported moderating rate hikes as early as February 2023. Meanwhile, 10-year Treasury yields declined and pressure on the dollar intensified, particularly after US retail sales posted their biggest drop in a year.

Obviously, traders are rejecting any hawkish comments from the Fed and are leaning toward a more dovish rhetoric suggesting that rates may soon be reduced.

Stock investors will continue to watch the reporting season this week. Oil giant Schlumberger Ltd. and financial services provider State Street Corp beat forecasts last week. This week, Google's parent company Alphabet Inc., which earlier cut thousands of jobs, is expected to release its financial results. Analysts expect the company's earnings to decline more sharply in Q4.

Japanese 10-year bond yields fell after the central bank took action to halt the yield increase by offering banks 1 trillion yen ($7.7 billion) in secured loans. Yields held at 0.375%, well below the 0.5% cap set by policymakers.

In other markets, crude oil declined as investors assessed demand prospects after China's reopening, as well as risks to production in Russia in 2023.

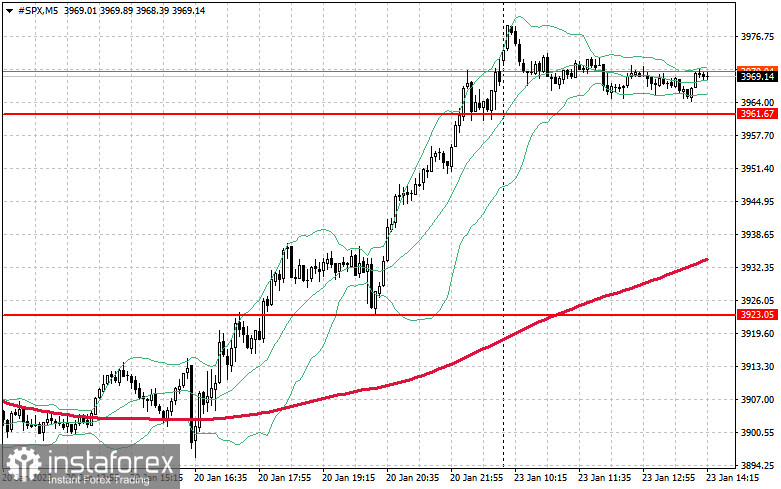

On the technical side, S&P 500 bulls continue to have the upper hand in the market. The index needs to hold on to its support level of $3,961 to extend its upside momentum. Furthermore, bulls will need to regain $3,983 to push the pair towards $4,010. Above this level lies $4,038, which will be a strong obstacle for the index. If the index moves down and bulls fail to prevent it from breaking below $3,960 and $3,923, it will quickly drop to $3,891.

InstaForex analytical reviews will make you fully aware of market trends! Being an InstaForex client, you are provided with a large number of free services for efficient trading.