Zostať

Zostať

Podmienky obchodovania

Nástroje

U.S. stock indexes rose on Tuesday, partially recouping losses from the previous session. Investors turned their attention back to the tech sector as attention shifts to upcoming inflation data and the start of the third-quarter earnings season.

The major indexes fell sharply earlier in the week amid rising Treasury yields, heightened geopolitical risks in the Middle East, and a reassessment of U.S. interest rate expectations. Each of the three major indexes lost about 1%.

However, falling bond yields sent the market into a buying frenzy on Tuesday, with attention once again focused on high-growth stocks that benefit from lower borrowing costs. As a result, investors increasingly bought shares of tech giants, which are traditionally sensitive to changes in the cost of capital.

The information technology sector led the S&P 500's gains, adding 2.1%. The biggest contributors were Palantir Technologies, which jumped 6.6%, and Palo Alto Networks, which gained 5.1%.

Among the "magnificent seven" tech titans, Nvidia has attracted particular attention. Its shares soared by 4.1%, recording the largest daily gain in the last month. Other tech giants such as Apple, Tesla and Meta Platforms (banned in Russia) were also in the green, adding between 1.4% and 1.8%.

Despite the positive mood, the Nasdaq and S&P 500 managed to rise only slightly compared to last week's levels. However, the tech sector continues to attract investors' attention amid expectations of new inflation data and corporate earnings reports that could set the direction of the market's future.

On Tuesday, US stock indexes once again demonstrated upward momentum, recouping some of the losses from the previous days.

The broad-based S&P 500 added 0.97%, rising 55.19 points to 5,751.13. Meanwhile, the tech-heavy Nasdaq Composite rose 1.45%, adding 259.01 points to 18,182.92. The Dow Jones Industrial Average also gained 126.13 points, or 0.30%, to end the day at 42,080.37.

Despite the positive momentum, investors continue to closely monitor any signals that could hint at the Federal Reserve's next steps in monetary policy. A decline in Treasury yields has been a catalyst for buying in the tech sector, but uncertainty around interest rates continues to dominate the market.

Throughout the year, market participants have been held hostage by the Fed, scrutinizing every macroeconomic report for hints of a possible policy shift. The main question on investors' minds is: when and at what speed will the Fed begin its long-awaited rate cuts?

Last week, economic data, including a stronger-than-expected employment report on Friday, forced the market to slightly revise its expectations. Investors began pricing in a lower probability of an aggressive rate cut. Instead of a 50 basis point cut, most analysts now expect the Fed to limit itself to a 25 basis point cut at its next meeting in November.

According to the CME FedWatch tool, traders are currently pricing in a nearly 89% chance of a 25 basis point rate cut in November.

The next big move in this "expectations game" will come on Thursday, when the CPI data is released. It is these numbers that will be critical to understanding the Fed's next moves and how soon the regulator will begin to ease its tight policy. Any deviation from the forecasts can immediately affect the behavior of markets and investor sentiment.

In any case, interest rates will remain the focus of market attention in the coming days, and any changes in macroeconomic data will be closely monitored to see which way the scales will tip – towards further easing or maintaining tight policy by the Fed.

Leading macroeconomic reports continue to be the focus of investors' attention, shaping expectations for the future policy of the US Federal Reserve. According to Jason Pride, head of investment strategy at Glenmede, it is the latest labor market data and the consumer price index (CPI) that will be the key benchmarks for the Fed ahead of their next meeting.

"If the CPI report comes in within the forecast range, this will be a signal for the regulator to limit the rate cut by 25 basis points in November," Pride said, commenting on the current expectations of market participants.

Amid the mixed movement of stocks on Tuesday, most sectors of the S&P 500 index ended the day in positive territory, but there were exceptions. Two sectors ended in the negative zone: materials and energy. The materials index (.SPLRCM) fell by 0.4%, which happened against the backdrop of a decline in metals prices. Investors lost optimism about possible measures to support the economy from the Chinese government, which led to a decrease in quotes in this segment.

Amid the general pessimism, shares of major Chinese companies listed on US exchanges also felt the pressure. For example, Alibaba Group, JD.com and PDD Holdings fell by 5.4%, 7.5% and 5.7%, respectively, following the decline of Chinese domestic indices.

The biggest losers were the energy sector (.SPNY), which fell by 2.6% - the largest daily drop since August 20. The reason is the correction in oil prices after their rapid rise at the beginning of the week. Concerns about slowing global demand and uncertainty around economic stimulus in China weakened support for oil, which was reflected in the quotations of energy companies.

Investors are also focusing on the third-quarter earnings season. This Friday, attention will be focused on large US banks, which will be the first to present their financial results. According to analysts at LSEG, the average earnings growth rate for S&P 500 companies is expected to be around 5%.

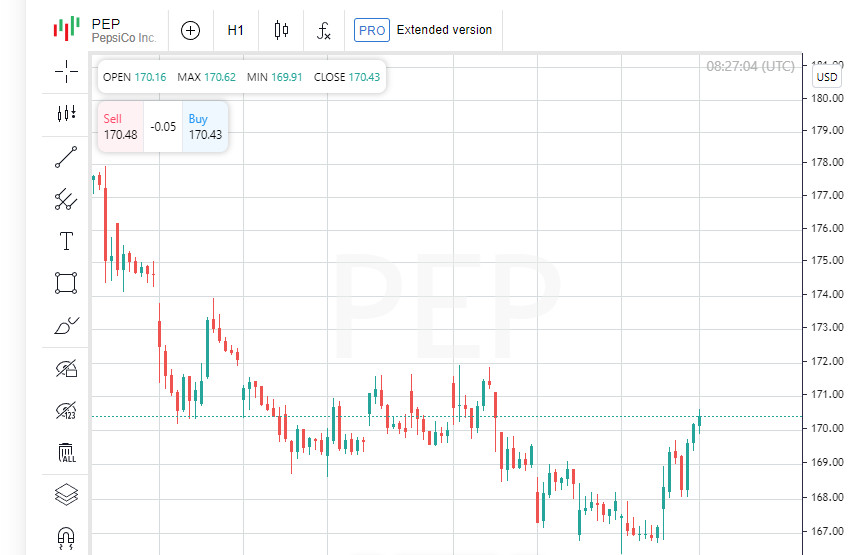

Among the companies that reported on Tuesday, PepsiCo stood out. The largest maker of beverages and snacks rose 1.9% after publishing adjusted earnings per share data that beat market expectations. Despite cutting its full-year sales growth forecast, investors took the company's results as a positive sign, which helped support the rise in its shares.

Amid growing interest in data and macroeconomic guidance, the market continues to balance expectations for Fed easing with concerns about global economic risks. The next earnings reports could be a determining factor for the future direction of stock markets.

US stock markets ended Tuesday on a positive note after the S&P 500 and Nasdaq posted strong gains. With geopolitical pressure easing and tech sector signals up, stock indexes were able to partially recover from their previous declines. Total trading volume on US exchanges was 11.57 billion shares, below the 20-session average of 12.1 billion shares.

The rally in global markets was largely driven by a rally on Wall Street, which was able to offset investor disappointment over the lack of concrete support measures from China. Market participants are eagerly awaiting details on possible stimulus measures, but for now their attention is shifted to upcoming macroeconomic reports in the US and the start of the quarterly earnings season.

US indices showed a confident rebound yesterday after falling by 1% the day before. A particularly powerful leap was recorded in the technology sector, where the S&P 500 (.SPX) added 0.97%, rising by 55.19 points, and closed at 5,751.13. In turn, the Nasdaq Composite (.IXIC) strengthened by 1.45%, jumping by 259.01 points and ending the session at 18,182.92. The Dow Jones Industrial Average (.DJI) added 0.30%, increasing by 126.13 points to 42,080.37.

The decline at the start of the week was caused by concerns about the escalation of the conflict in the Middle East and a reassessment of expectations for the Fed's monetary policy. Strong data on the US labor market, published on Friday, increased concerns that the Fed will not rush to ease its policy, which led to a decrease in risk appetite among investors.

All attention is now focused on fresh inflation data, which will be published on Thursday. The consumer price index (CPI) will be an important marker for determining the future direction of the Federal Reserve's monetary policy. If inflation turns out to be higher than expected, this could reinforce current expectations that the Fed will take a tougher stance on interest rates.

Investors are also preparing for the start of the corporate reporting season. The largest US banks, which are traditionally the first to disclose their financial results, will give the start later this week. Attention will be focused on their comments on the state of the economy and the outlook for the monetary policy shift.

With US indices recovering and geopolitical concerns easing, investor sentiment remains heavily dependent on upcoming macroeconomic data and corporate earnings. Inflation, the labour market and the Fed's strategy will all shape the trading dynamics in the coming weeks, impacting investors' appetite for risk assets and, therefore, the sustainability of the current rally.

European stock indices ended lower on Tuesday as investors were disappointed by the lack of concrete details on China's new fiscal stimulus. Market expectations were not met, leading to a fall in stocks focused on Chinese demand, such as miners and luxury goods makers.

MSCI's global share index showed a small gain, rising 0.15% to 844.96 points, thanks to a partial recovery in the US and Asian markets. However, the pan-European STOXX 600 index fell 0.55%, reflecting the general mood of pessimism on the continental markets.

The main disappointment was the dynamics of Hong Kong's Hang Seng, which fell by 9.4% - the largest drop since 2008. This happened after the head of China's National Development and Reform Commission Zheng Shanjie, who assured that the country's economy is "confidently" moving towards its goals for 2024. Moreover, he noted that the authorities intend to direct 200 billion yuan (about 28.36 billion US dollars) to support regional projects and investment in infrastructure. However, investors were expecting much more, as the lack of concrete steps and new support measures has raised doubts about Beijing's ability to effectively counter the current economic downturn.

After the end of the national holidays, Chinese stock indices such as the Shanghai Composite and CSI300 showed sharp declines, falling by 4.6% and 5.9%, respectively. These losses effectively "ate up" a significant part of recent gains accumulated amid expectations of a large-scale economic stimulus. The decline in indices was a response to the uncertainty surrounding the Chinese government's plans and the lack of clear signals about further economic stimulus.

Meanwhile, the US Treasury market saw a slight decline in yields, reflecting investor caution in an uncertain environment. Market participants continue to closely monitor the Federal Reserve's signals, trying to understand how macroeconomic data and the regulator's positioning will affect the trajectory of interest rates.

Amid a general decline in stock markets, investors have adopted a wait-and-see attitude. The focus remains on the upcoming inflation and corporate profit reports in the US. In the coming days, it is these data that will determine the further direction of both US and international indices. Any surprises, be they positive or negative, could trigger significant changes in the markets, especially against the backdrop of fragile confidence in the prospects for China's economic recovery.

While markets are looking for new reference points, the issue of trust in the actions of central banks and governments comes to the fore: their decisions can either support investor sentiment or exacerbate volatility in financial markets.

According to the latest data from the CME FedWatch Tool, the probability of the Federal Reserve cutting rates by 25 basis points in November is estimated at 87.3%. However, there is still a small chance - 12.7% - that the Fed will choose to leave rates unchanged. Just a week ago, the market had a different view: expectations for a rate cut were almost fully priced in, but uncertainty about the size of the next step has reduced the likelihood of a more aggressive easing by 50 basis points.

The yield on the 10-year US Treasury note, a key benchmark for markets, fell by 0.6 basis points to 4.02%. Such a small change indicates continued caution amid ongoing speculation about the Fed's next steps and the macroeconomic situation in the country.

After the recent rally triggered by geopolitical risks, oil prices have sharply corrected downwards. The main driver of the decline is easing concerns about supply disruptions amid the military standoff in the Middle East and improving weather conditions in the Gulf of Mexico. U.S. WTI crude lost 4.63% to $73.57 a barrel, while Brent crude also fell 4.63% to close at $77.18 a barrel.

Military tensions in the Middle East continue, weighing on global markets. Israeli Prime Minister Benjamin Netanyahu announced that airstrikes had killed two key successors to the slain Hezbollah leader, in the latest escalation of the conflict. Meanwhile, the group's deputy leader left the door open for ceasefire talks, raising hopes for a possible easing of tensions. The comments came just hours after Israel expanded its offensive against Iran-backed militias.

The dollar index, which tracks the dollar against a basket of six major currencies, was unchanged, closing at 102.48. Meanwhile, the euro showed a slight strengthening, adding 0.04% to $1.0978. The Japanese yen weakened by 0.07%, and the dollar rose to 148.29 yen per unit of the American currency. In contrast, the pound sterling strengthened by 0.13%, rising to $1.31, demonstrating confidence amid relative stability in European markets.

The current fluctuations in financial markets reflect the ambivalent mood of investors. Amid geopolitical tensions and volatile commodity markets, traders' attention is shifting to macroeconomic reports and upcoming central bank meetings. The publication of US inflation data and further signals from the Fed could become catalysts for both further growth and a new round of volatility on global markets.

InstaForex analytical reviews will make you fully aware of market trends! Being an InstaForex client, you are provided with a large number of free services for efficient trading.