Zostať

Zostať

Podmienky obchodovania

Nástroje

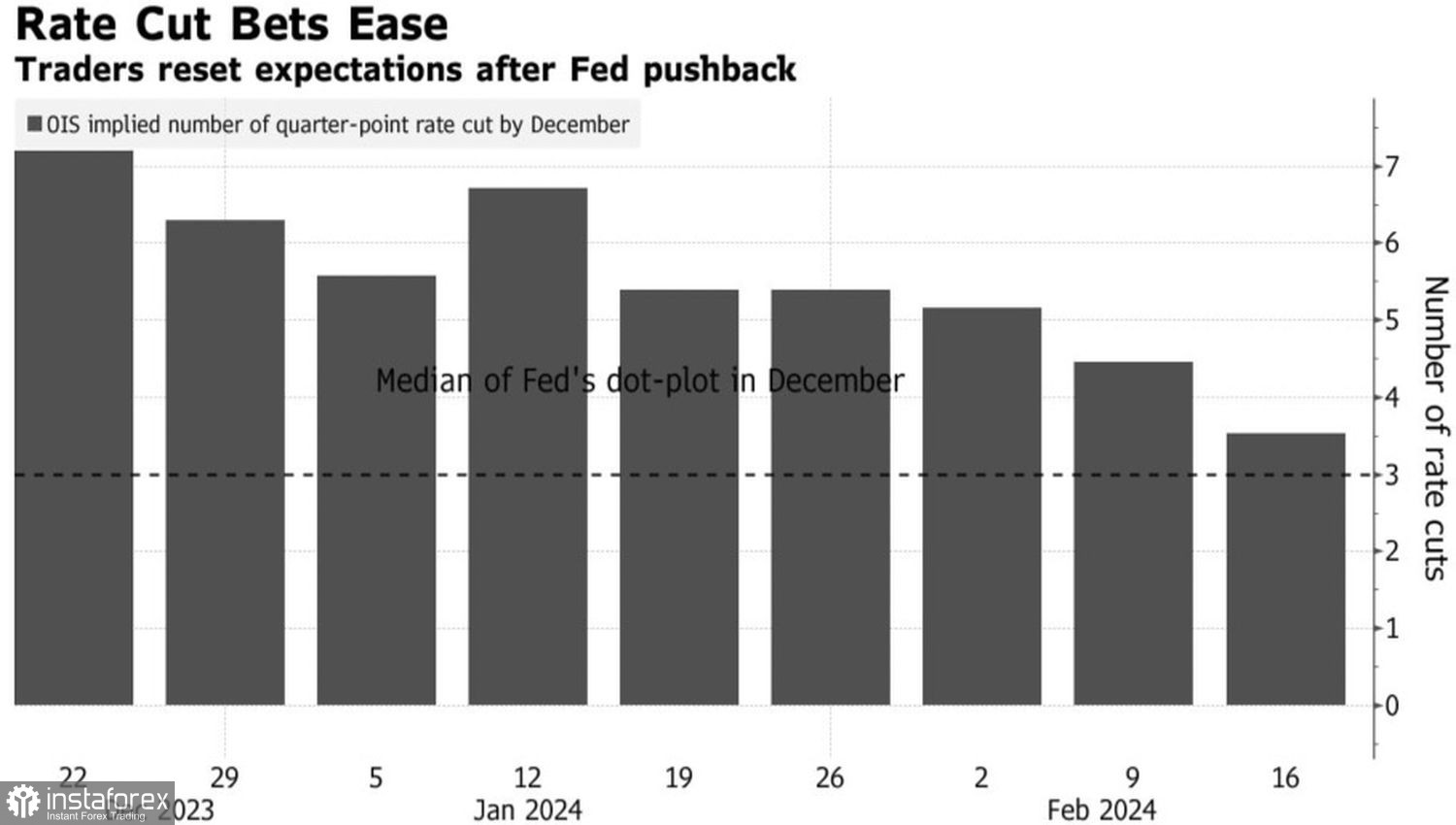

Not too long ago, the market was confident that the Federal Reserve System would lower the federal funds rate in 2024 over six FOMC meetings. Chairman Jerome Powell was even forced to express his dissatisfaction with investors' forecasts of the start of monetary expansion in March. Now, they are choosing between three and four Committee meetings. Moreover, options have emerged, foreseeing an increase in borrowing costs from current levels or after a decrease by 25–75 basis points. Each of them instills optimism in the bears on EUR/USD; however, confirming data is needed for their implementation.

Throughout most of the Fed's tightening cycle in 2022–2023, investors recalled the example of the 1970s when premature declaration of victory over inflation resulted in a double recession. At the end of winter, analogies are drawn with another story. In 1998, the Central Bank lowered the federal funds rate in response to the financial crisis triggered by the Russian default and the collapse of the Long-Term Capital Management hedge fund. However, starting from June 1999, the Federal Reserve initiated a cycle of tightening monetary policy to curb high inflation.

Investors' bets on Fed's monetary policy options

The persistent reluctance of the U.S. economy to undergo a soft landing may reignite prices with renewed vigor. As a result, the Fed will be forced to keep borrowing costs at a plateau longer than expected. For instance, Nordea Markets forecasts that in 2024, investors will see only two reductions in the federal funds rate to 5%. Societe Generale even believes that the acceleration of the U.S. GDP will compel the Fed to return to tightening monetary policy. As a result, the U.S. dollar will return to its peak levels seen in 2022.

For the Federal Reserve and the entire financial market, it is crucial to understand why the pace of Gross Domestic Product (GDP) growth is increasing at the moment. If it is about the delayed effects of monetary restriction or a temporary impulse due to the recovery of supply chains, the economy is likely to slow down soon. Then the scenario of further inflation slowdown and the start of Fed's monetary policy easing in June may unfold.

Market forecasts for the number of acts of Fed's monetary expansion

On the contrary, if GDP acceleration is not a temporary phenomenon, but factors such as emigration, an increase in the military industry due to armed conflicts in Eastern Europe and the Middle East, and increased productivity through the implementation of artificial intelligence technologies drive GDP, the Central Bank will have to act differently.

Judging by the rally in EUR/USD, investors prefer the first scenario, where the economy and inflation are slowing down. The U.S. dollar has played out its main trumps. For now, there is no rush to close long positions in the American currency.

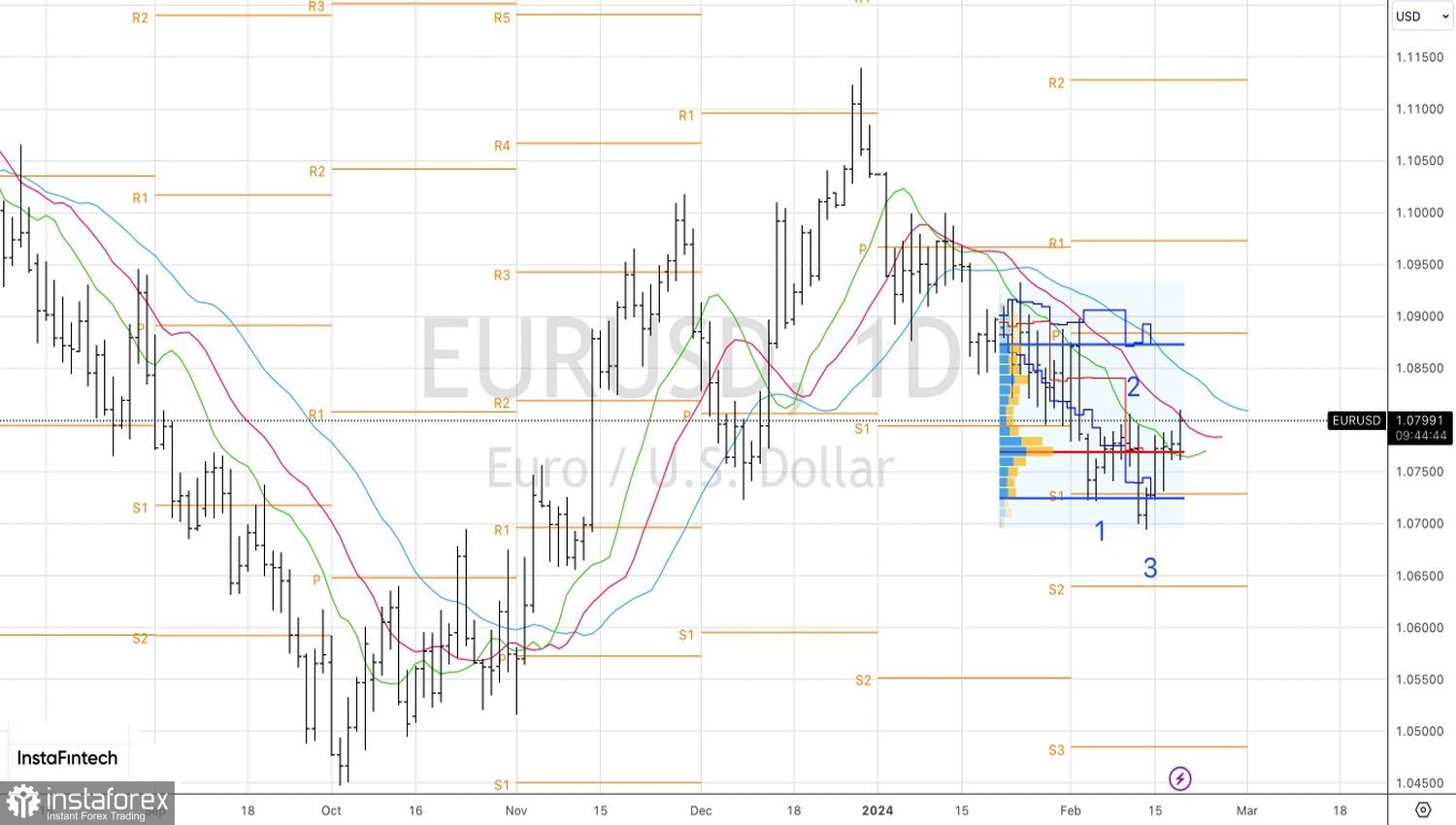

Technically, on the daily chart, EUR/USD is playing out the 1-2-3 pattern. Long positions formed on the breakthrough of resistance at 1.079 make sense to hold and increase towards 1.084 and 1.088.

InstaForex analytical reviews will make you fully aware of market trends! Being an InstaForex client, you are provided with a large number of free services for efficient trading.